Crypto Exchange Australia

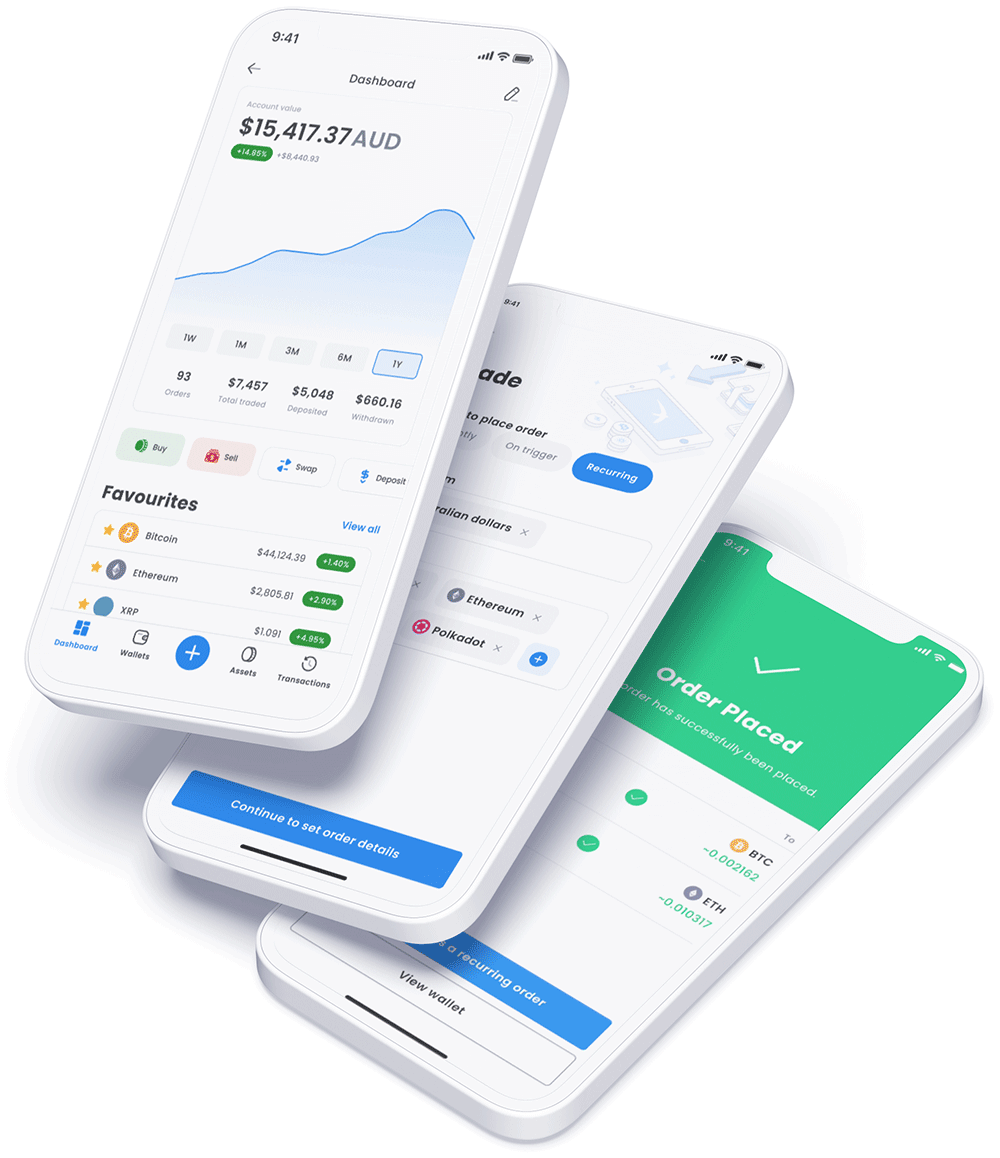

Buy crypto in minutes

- Signup for free

- Verify your account

- Fast AUD Deposits

- Start trading 320+ cryptocurrencies

Official partner of

![]() withdrawals & deposits

withdrawals & deposits

owned and operated

assets for trading

on ![]() *

*

Swyftx is an AUSTRAC registered digital currency exchange headquartered in Brisbane, Australia.

Swyftx holds ISO27001 certification which is internationally recognised for information security.

Your assets and funds are protected through multi-layer technology and advanced security frameworks.

Our Australian-based support team are here to answer all your questions and help you navigate the Swyftx platform.

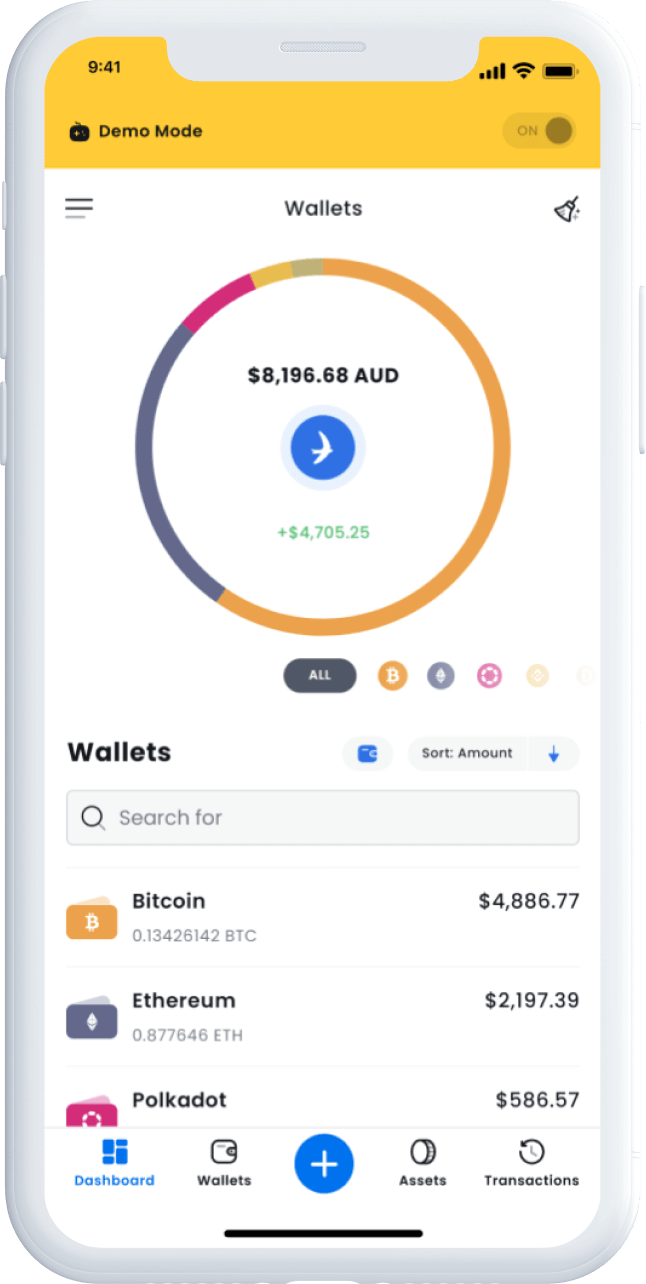

Test your strategies and learn the market without committing your own money with our demo mode.

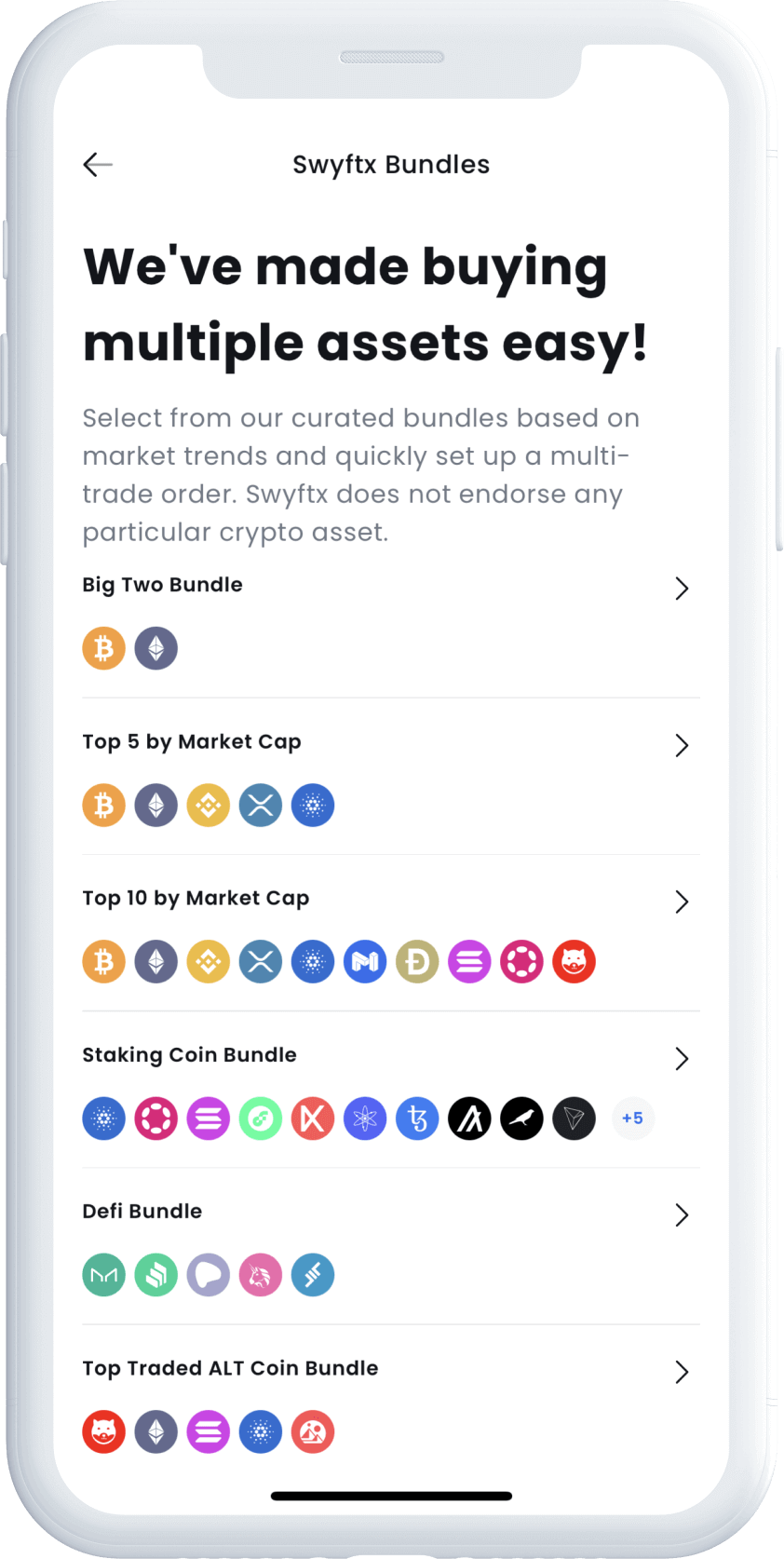

Diversify your cryptocurrency portfolio and purchase multiple assets with just one single trade.

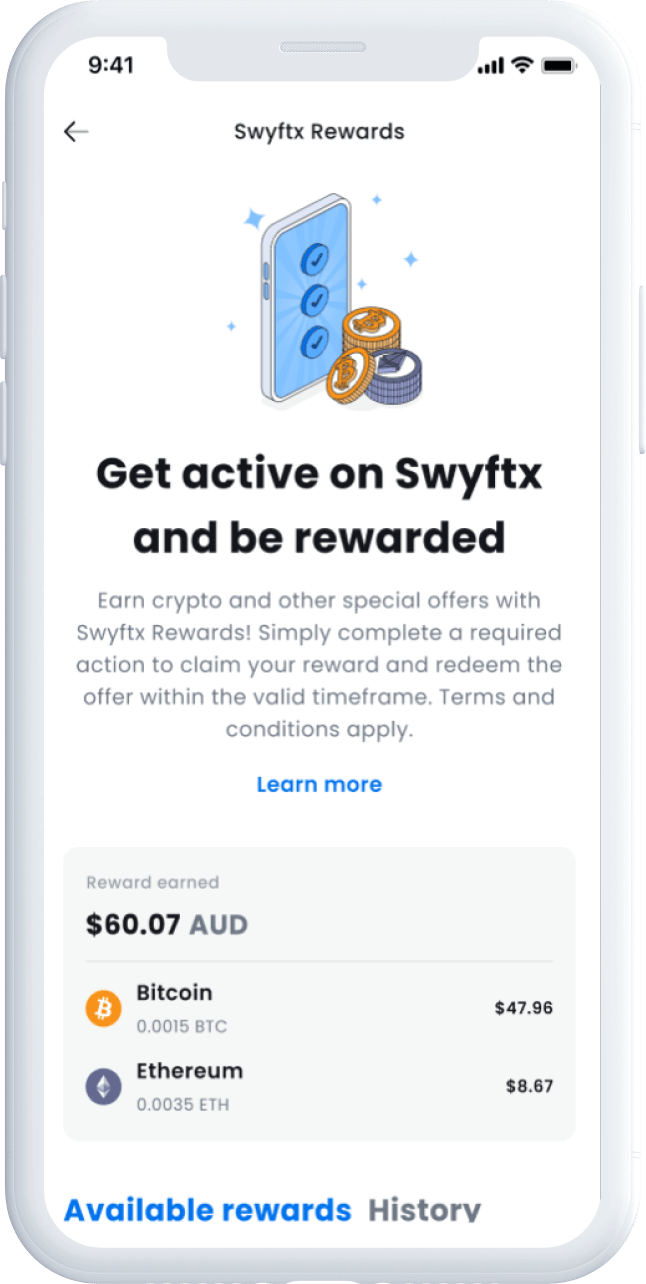

Be rewarded with crypto and other special offers by actioning certain tasks within the Swyftx platform.

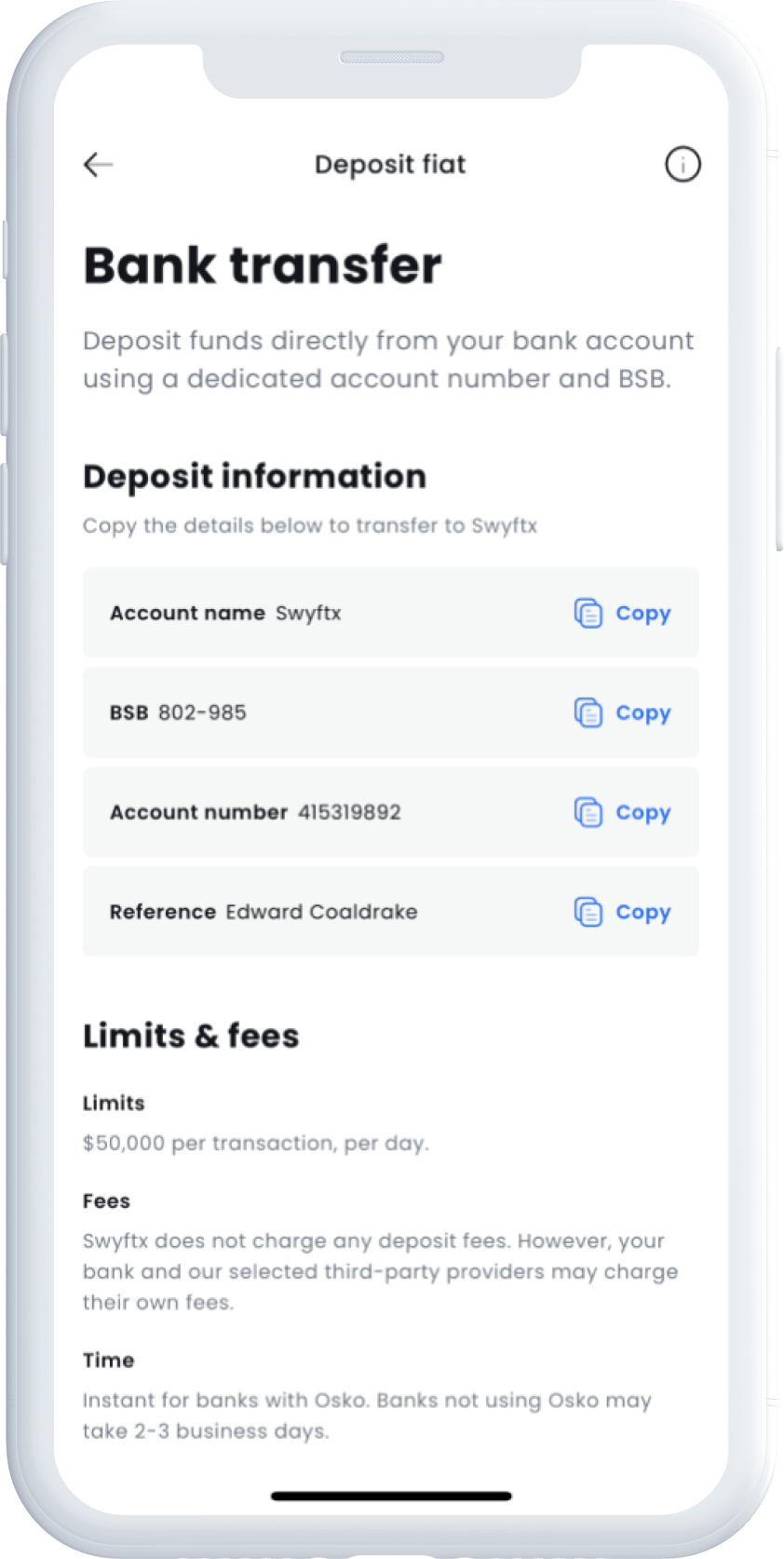

Deposit funds easily into your account via a number of payment methods, some of which are processed instantly.

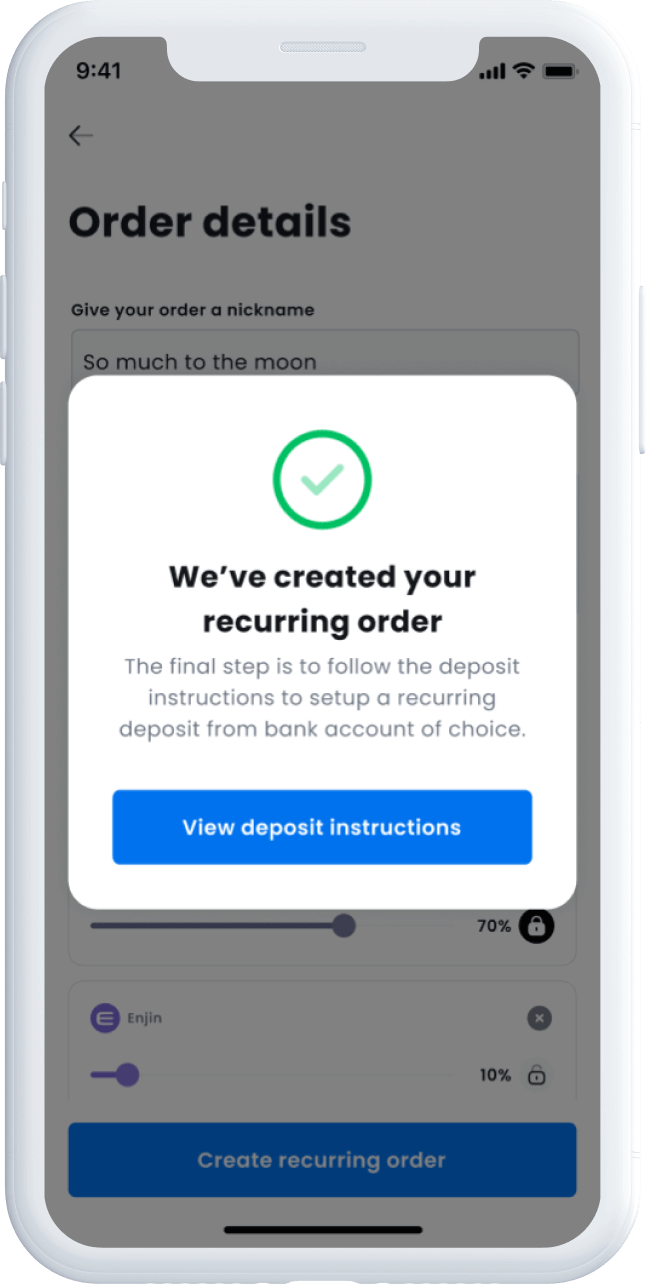

Set up recurring deposits and have orders automatically trigger across a range of assets.

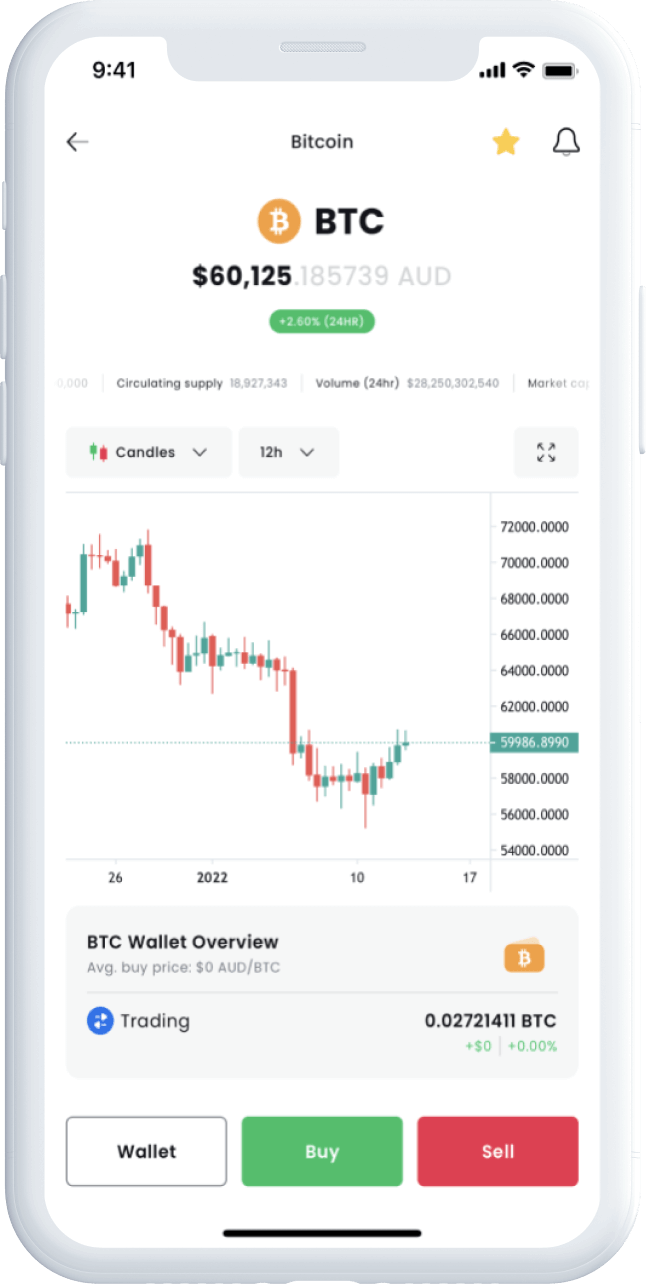

Utilise technical indicators and tools to track and analyse your preferred assets with our TradingView charts.

Stay up to date on the latest news and trends in the market by accessing real-time news from numerous publications.

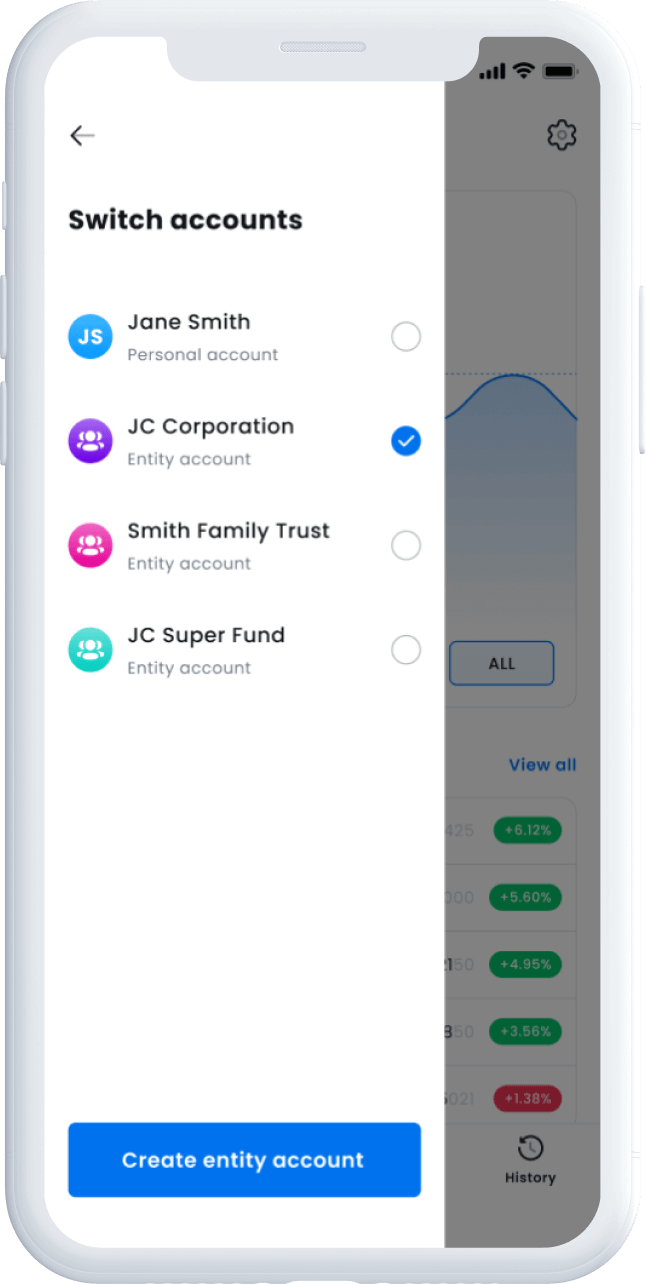

Invest in cryptocurrencies through your company, trust, or SMSF and keep track of your investments in a single location.

*Excellent

4609 Reviews on

Very good customer support. Overall efficiency is very good

Easy to use, buy and sell 😀

I have used Ds Cs, BTCm. Swytx it has become my favourite platform. It takes a while to get adjusted. I like the multiple selling and swap make thin...

It’s a great app to navigate, they have good variety of coins to invest in. I’m very happy with my experience with Swyftx at the moment

Excellent customer service and an easy platform to use when starting to invest.

The best crypto wallet in Australia The customer service team are the best to solve your problems for you,I really appreciate their service and I c...

I have been using Swyftx app to buy my first cryptocurrency. The interface is awesome, very clear and useable. It has made it an easy transition into ...

I began my investing journey with swyftx and as an absolute beginner to crypto swyftx took the worry out of investing for me its simple and easy to us...

Great customer service, easy to use interface and an unwavering confidence that they are doing things “right” and above board means SwyftX is the ...

Quite user friendly and easy to use, especially as an Australian because Swyftx links to tax office which makes our taxation related activity easier. ...

View detailed “how to” guides and instructions on navigating the Swyftx platform and using specific features.

Send your question via live chat and we’ll reply with a helpful answer - under 10 minutes.

Access quality educational resources and expert market analysis to sharpen your crypto and blockchain knowledge.

Listen to the Tapping into Crypto podcast for the latest trends and opportunities in cryptocurrency.